Kobo by Kobo: The Silent Siphon Draining Nigeria’s Bank Accounts

ABUJA, Nigeria – The alert tone is now part of Nigeria’s daily rhythm — a soft ping that signals money received or sent. For millions, it is the sound of convenience, of a rapidly digitising economy where cash is no longer king. But beneath that reassuring chime lies a quieter, more insidious pattern: a steady drip of charges that, over time, quietly erode personal finances.

Across Nigeria, the shift to digital banking has transformed how money moves. Transfers are instant, payments seamless, and Point-of-Sale terminals ubiquitous. Yet, as the country embraces this convenience, many customers are beginning to confront an uncomfortable question: how much does it really cost to use your own money?

What appears trivial — ₦10 here, ₦50 there — is increasingly becoming a source of unease. Individually negligible, collectively consequential, these micro-charges are drawing scrutiny from customers who say the cumulative impact is anything but small.

The Hidden Weight of Small Deductions

For many Nigerians, the realisation does not come immediately. It creeps in slowly — often during a rare moment of financial reflection.

“I didn’t take it seriously at first,” said Mrs. Ngozi Eze, a secondary school teacher in Abuja. “But when I checked properly, I realised I had spent over ₦3,000 in one month on different bank charges alone. That’s money I didn’t plan for.”

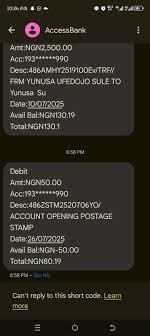

Her experience is far from isolated. A closer look at bank statements reveals a web of deductions: transfer fees, SMS alerts, ATM withdrawals, card maintenance charges — each individually modest, but collectively significant.

“Each one looks small, but together, it’s a lot,” she said. “You just see alerts coming in, and before you know it, your balance has dropped.”

The invisibility of these deductions — their ability to blend into the background of everyday transactions — is precisely what makes them powerful. They rarely trigger alarm in isolation, but over time, they reshape spending power in subtle ways.

Traders Count the Cost

In Nigeria’s bustling informal economy, where margins are thin and transactions frequent, the effects are even more pronounced.

At Wuse Market in Abuja, Mr. Ibrahim Sani has watched his business evolve alongside the country’s payment habits. Cash, once dominant, is steadily giving way to transfers.

“Customers rarely bring cash now. They prefer transfers, which is fine,” he said. “But I receive payments many times a day. When I move the money or withdraw it, charges follow.”

For traders like Sani, the issue is not merely about inconvenience — it is about survival in a competitive marketplace.

“At the end of the week, you will see that the money is not complete,” he said. “The charges have already taken part of it.”

He also pointed to another layer of disruption: failed transactions.

“Sometimes money is deducted, but the person I’m paying doesn’t get it immediately. You have to wait for a reversal, and that can delay business.”

In a system where speed is supposed to be the selling point, such delays carry real economic consequences.

Salary Earners Feel the Pinch

For salaried workers, the pattern is different but no less frustrating. The issue is not frequency, but inevitability.

Miss Blessing Okafor, a civil servant in Abuja, described a familiar cycle that begins the moment her salary is credited.

“The moment my salary enters, deductions start — card maintenance, account maintenance, SMS charges,” she said. “It feels like you’re being charged just to keep your money in the bank.”

The opacity of some deductions adds to the frustration.

“Sometimes the descriptions are not clear. You have to go through everything carefully before you understand what happened.”

For many, this lack of clarity deepens a sense of mistrust — a feeling that the system operates just beyond full comprehension.

Inside the Banking System

From within the industry, bankers insist that the charges are neither arbitrary nor exploitative, but structured and regulated.

Mr. Daniel Adeyemi, a commercial banker with UBA in Abuja, said most fees are guided by official policies.

“These fees are guided by regulatory policies,” he explained. “Banks incur costs maintaining digital platforms, processing transactions, and securing customer data. Charges help cover those expenses.”

Yet even he acknowledged a communication gap.

“One of the biggest issues is that customers don’t always understand what they are being charged for. Banks need to do more in terms of transparency and education.”

Adeyemi argued that digital banking has eliminated other burdens — long queues, transport costs, and hours spent in banking halls. But the trade-off, he admitted, is a higher frequency of charges.

“That’s what customers are reacting to,” he said.

A New Revenue Model

Beyond operational costs, analysts say the proliferation of small charges reflects a deeper shift in how banks generate income.

“Banks are now earning more from transactions than before,” said financial analyst Mr. Tunde Balogun. “Every transfer, every alert, every card payment contributes to their revenue.”

This transaction-driven model, he explained, is reshaping the financial landscape.

“For high-income earners, these charges may not mean much. But for low- and middle-income earners, they can take a real toll over time.”

Balogun stressed that the real issue is not just the charges themselves, but the lack of awareness.

“Many people don’t track these deductions closely. If they did, they would realise how much they are losing monthly.”

Regulation Meets Reality

In principle, bank charges in Nigeria are not unregulated. They are governed by official guidelines designed to standardise fees and protect consumers.

In practice, however, awareness remains low.

“There is a gap between policy and public understanding,” Balogun said. “Customers need more information about their rights and the approved charges.”

Without that knowledge, customers are left navigating a system they do not fully understand — one where questioning deduction becomes difficult, and accountability remains limited.

The Cost of Convenience

Nigeria’s push towards a cashless economy is widely seen as a step forward — improving efficiency, transparency, and financial inclusion. But as digital adoption accelerates, so too does scrutiny of its hidden costs.

“I don’t mind paying for services,” Mrs. Eze said. “But I want to know exactly what I’m paying for. It shouldn’t feel like money is disappearing without explanation.”

Her words capture a broader sentiment: that convenience, while valuable, should not come at the expense of clarity and fairness.

A System Under Question

As millions of Nigerians continue to rely on digital banking, the conversation is shifting. What was once accepted as a minor inconvenience is now being re-examined as a structural issue.

The challenge ahead lies in balancing innovation with accountability — ensuring that financial systems remain both sustainable for providers and fair to users.

For now, the deductions continue — quiet, routine, almost invisible. But their cumulative impact is becoming harder to ignore.

Kobo by kobo, they tell a story not just of banking, but of trust — and of a system that must decide how much that trust is worth.